Mish's Global Economic Trend Analysis |

| Posted: 24 Oct 2014 12:54 PM PDT Things are about to get more interesting in the EU as a review of budget procedures shows the UK, Greece, and Italy owe more money, but Germany and France will get money back. Curiously, this came about following a review of non-profit organizations from churches and universities to trade unions, charities and sports clubs. The time period is 2002-2009. Cameron's Obvious Bluff UK prime minister David Cameron is already battling French President Francois Hollande abroad, and UKIP at home. Thus, Cameron's limited choice is to bluff as usual: "We Won't Pay," Says Furious Cameron. In a vivid display of public fury at European Union technocrats, British Prime Minister David Cameron refused to pay a surprise 2.1-billion-euro bill on Friday as EU leaders ordered an urgent review of how the budget figures were arrived at.Hyperventilation Charade It's easy to see through Cameron's hyperventilation charade. Cameron did not really say "We won't pay" as the Reuters headline states. Rather, Cameron stated "I'm not paying that bill on Dec. 1". The latter statement would be true if Cameron paid the bill on any date before or after December 1, or the amount changed by a penny. This is the kind of wishy-washy nonsense that Cameron pulls all the time. Unfortunately, conservative believers fall for it every time. Similarly, Cameron promises an up-down vote on UK membership in the EU, but only if he is reelected. Would he even keep that promise? Who the hell knows? Cameron's pledge is to first get the EU to change its rules more to the UK's liking. If he succeeds, then and only then will he offer the vote (and of course he has to win reelection on top of it). Odds Cameron gets the rule changes he seeks are approximately 0%. You know it, I know it, the world knows it, and even Cameron knows it. The promise of a 2017 up-down vote is nothing more than an election ploy coupled with blatant arrogance. Liar, Not a Conservative As I have stated before, Cameron is a liar, not a conservative. He is in a coalition bed with the Liberal-Democrats, a pro-euro, pro-Labour, pro-climate-change, free education, and progressive tax party. With that set of bed-mates, no conservative in their right mind should believe a damn thing he claims to stand for. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

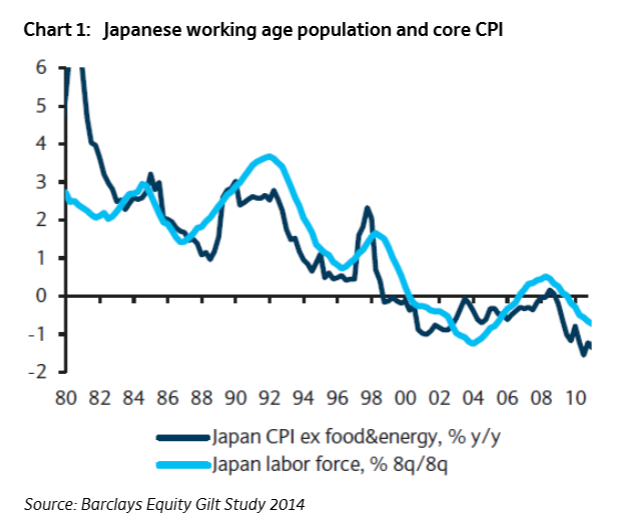

| Japanese Style Deflation Coming? Where? Fed Falling Behind the Curve? Which Way? Posted: 24 Oct 2014 10:05 AM PDT There's some interesting discussion points in the UK-based Absolute Return Partners October 2014 Letter, by Niels C. Jensen, most of which I agree with, others not. Japan-Style Deflation in Our Backyard?Deflation and "Willingness To Do Something" Jensen is mistaken about Japan's willingness to take action. Japan has a debt-to-GDP ratio of 250%, highest of any major developed country, as a direct consequence of fighting deflation. Japan piled on debt, built bridges to nowhere, and engaged in other wasteful spending, all of which made matters worse. Taking on debt to fight deflation is insane. Yet that is exactly what France and Italy want now! Japan's QE certainly did not help either. Both policies addicted Japan to 0% interest rates forever (until of course Japan blows up). To suggest that the ECB can do something meaningful with European demographics being what they are, the flaws in the euro being what they are, and lack of willingness for France and Italy to initiate badly-needed structural reforms, is simply wrong. Holding down interest rates and state-sponsored stimulus will have the identical result as in Japan. As for wages, they are actually rising not only in the US, but also in Europe as I pointed out in European Service Prices Plunge at Steepest Rate Since January 2010; Reflections on Keynesian Stupidity. In the US, the Fed did stave off for now, another round of price deflation. However, that came at the expense of creating monstrous asset bubbles. The bursting of asset bubbles is inherently deflationary, and much more damaging than falling prices because of the impact asset prices have on asset-based loans. I propose falling prices should be welcome across the board. Behind the Curve? Is the Fed Falling Behind the Curve?Behind the Curve? Which Way? Curiously, St. Louis Fed Governor James Bullard says Fed Should Consider Delay in Ending QE because "Inflation expectations are declining in the U.S." That's nonsense of course because of the asset bubbles the Fed spawned. With interest rates so low across the world, the chase for yield is on. Opportunity in Japan Which Equity Markets Offer Most Potential?Japanese Equities and the Yen It's certainly debatable whether Japan has turned the corner economically. Nonetheless, on a valuation basis alone, I have been recommending a yen-hedged position in Japanese equities. Whether or not the Yen plunges will have to do with Abenomics, and how Japan eventually handles (or doesn't) zero percent rates. Jensen's comment that US equities are "more or less fully priced" is silly. US equities are priced well beyond perfection in one of the biggest valuation bubbles in history. Pension Fund Piling On Jensen concludes with an interesting chart and comments about piling on. Investors (well, most investors) continue to pile in to equities, as if they are the solution to their return challenge.Disconnects I agree with Jensen on Japanese equities, hedging the Yen, and the prospects of deflation in Europe. The chart on asset allocations is particularly interesting. Investors are overweight equities just as they were were in 2000 and 2007, and I believe with dire consequences. Jensen says "Statistically, equity markets fall 40-50% (as they did in 2008-09) only a couple of times in a life time, so why somebody is forecasting the next bloodbath to be around the corner is quite frankly beyond me." It seems to me that equities plunged in 2000 and again in 2007. So that was twice in a seven year timespan. Given valuations are equally extreme now, caution is more than in order. Japan prove stocks can stay depressed for decades. And that can happen again, someplace else, besides Japan. Central Bank Action I disagree with Jensen on the need for the ECB to do anything about falling prices. For discussion, please see Challenge to Keynesians "Prove Rising Prices Provide an Overall Economic Benefit". Inquiring minds may also wish to consider James Grant Conference Video: Inflation Expectations, Growth, Policy Problems; Europe Has Become Japan. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment