| Rational Reason to Panic; Hot Money Blues; Right for the Wrong Reasons Posted: 27 Mar 2013 11:06 PM PDT The first rule of panic is simple: " Panic before everyone else does." With that rule in mind, the obvious question is likewise simple: " Should I panic now?" For those in Europe, I offer an emphatic " Yes!" One is foolish at best to keep more than 100,000 euros in any European bank, especially any Southern European banks. Nonetheless, fools are everywhere, even though there is a clear and obvious " Rational Reason to Panic". I am not the only one who thinks that way. Wolfgang Münchau makes the case in his Der Spiegel column Euro rescue plan: Thank Dijsselbloem! Dutch Finance Minister and Euro Group Chief, Jeroen Dijsselbloem earned much criticism because he deviated from the official line that Cyprus was an "isolated incident".

I welcome this unusual burst of openness. Dijsselbloem expressed the brutal truth. I'm not criticizing that he states the policy. Rather, I criticize the policy itself.

This policy will destroy the euro, with the two now foreseeable interlocking mechanisms.

The first way is capital flight from the euro crisis countries. Expect permanent restrictions on the free movement of capital.

The second way is a never ending recession in the eurozone.

The first of these mechanisms is the logical consequence of Dijsselbloem's settlement blueprint. Spanish or Portuguese citizens would be pretty stupid to keep over 100,000 euros in a savings account.

Rational savers will distribute their assets to different banks, each with a limit of €100,000. German savers will do so as well.

Germany rejects a European deposit guarantee, so no credible reinsurance exists across southern Europe. Most of the Southern states are insolvent. A Cyprus-like rescue works only in context of a union of banks, and Germany emphatically rejects that mechanism.

Dijsselbloem's blueprint and Germany's veto of a European deposit guarantees savers have a "rational reason to panic now", everywhere.

The Withdrawal Debate Has Begun

US economist Paul Krugman says that it now is the best for Cyprus to leave the euro.

Cyprus is officially an "isolated incident". Greece, Spain, and Portugal will be there as well. Dijsselbloem's dictum guarantees that end. And Because there are proportionally fewer large savers in Spain than Cyprus, the hazard on a participation of small savers is even greater.

Expect bank runs or permanent controls on capital flows. Either way, the Monetary Union will come to an end. Right for the Wrong Reasons Reader Bernd, from Germany, sent me the above link. I translated it, hopefully accurately, with a copy of this post going to Wolfgang Münchau. In his email, Bernd says... Paul Krugman has advised Cyprus to exit the Eurozone. You advised Cyprus the same, for the right reasons. Krugman does so, for the wrong reasons. I hope the day comes, when Münchau quotes you instead of Krugman.

Bernd Hot Money Blues Münchau and Bernd refer to Hot Money Blues by Paul Krugman. Whatever the final outcome in the Cyprus crisis — we know it's going to be ugly; we just don't know exactly what form the ugliness will take — one thing seems certain: for the time being, and probably for years to come, the island nation will have to maintain fairly draconian controls on the movement of capital in and out of the country.

Depending on exactly how this plays out, Cypriot capital controls may well have the blessing of the International Monetary Fund, which has already supported such controls in Iceland.

It's hard to imagine now, but for more than three decades after World War II financial crises of the kind we've lately become so familiar with hardly ever happened. Since 1980, however, the roster has been impressive: Mexico, Brazil, Argentina and Chile in 1982. Sweden and Finland in 1991. Mexico again in 1995. Thailand, Malaysia, Indonesia and Korea in 1998. Argentina again in 2002. And, of course, the more recent run of disasters: Iceland, Ireland, Greece, Portugal, Spain, Italy, Cyprus.

What's the common theme in these episodes? Conventional wisdom blames fiscal profligacy — but in this whole list, that story fits only one country, Greece. Runaway bankers are a better story; they played a role in a number of these crises, from Chile to Sweden to Cyprus. But the best predictor of crisis is large inflows of foreign money: in all but a couple of the cases I just mentioned, the foundation for crisis was laid by a rush of foreign investors into a country, followed by a sudden rush out.

Now what? I don't expect to see a wholesale, sudden rejection of the idea that money should be free to go wherever it wants, whenever it wants. There may well, however, be a process of erosion, as governments intervene to limit both the pace at which money comes in and the rate at which it goes out. Global capitalism is, arguably, on track to become substantially less global.

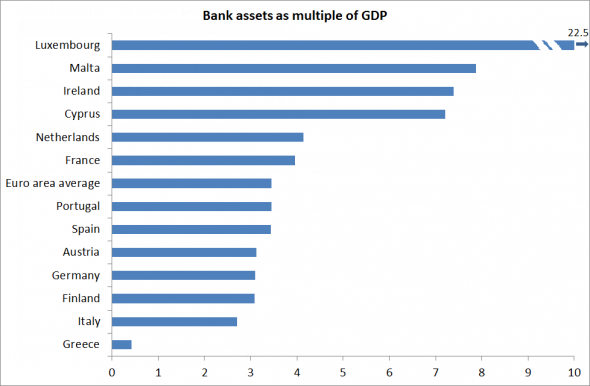

And that's O.K. Right now, the bad old days when it wasn't that easy to move lots of money across borders are looking pretty good. 85% Rubbish As is typically the case (which explains his popularity), Krugman gets part of the story correct, the sensational part. Krugman is of course correct that Cyprus is going to be ugly. And he is sure to follow up with numerous "I told you so" articles. This is where common sense stops and nonsense begins. Europe and the US do not suffer from lack of capital controls. The origin of this crisis is fractional reserve banking in and of itself. The Krugman "solution" is more government controls, more taxation, more regulation, more manipulation, even to the point of actually advocating the "bad old days" when everyone had capital controls. In addition to capital controls, Krugman advocates tariffs, advocates higher minimum wages, higher taxes, and more government spending. Good grief! Not once does Krugman ever stop and think that the absurd Keynesian policies that he espouses are precisely what has caused the problem! Capital flight starts because of the nonsensical policies he espouses. Money flows to places like Cyprus, Luxembourg, and Spain "because of " inane Keynesian and Monetarist problems elsewhere. Rather than address the root problems, Krugman now wants capital controls on top of all the other idiotic things he desires. When does it stop Paul? When? Reflections on Münchau's Shift in Attitude I believe Münchau's heart is in the right place. He really wanted to make the eurozone work, believing the euro would help create a better Europe. However, the eurozone can never work. The euro was fatally flawed from the beginning, starting with a " one size fits Germany" interest rate policy and lack of appropriate banking unions. The global recession brought those flaws to the forefront, and the North-South divide is the widest ever, and growing. To no surprise (at least in this corner) euro skepticism is large and growing in the UK, Italy, Greece, and Poland. Cyprus and Spain will soon follow. Meanwhile, attitudes in Germany and the Netherlands make it impossible for there ever to be the union that Münchau once envisioned. It is extremely refreshing to see Münchau questioning ideas he once held sacrosanct. For that reason I commend Münchau, even though quoting Krugman for the wrong reasons can hardly be commended at all. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Wine Country Conference I am hosting an economic conference on April 5 in Sonoma, California. Proceeds go to the Les Turner ALS Foundation (Lou Gehrig's Disease). Please see My Wife Joanne Has Passed Away; Stop and Smell the Lilacs for my association with the disease. To learn about the economic conference with world-class speakers including John Hussman, Michael Pettis, Jim Chanos, John Mauldin, Mike "Mish" Shedlock, Chris Martenson with guest moderator Lauren Lyster and other Special Guests, please visit Wine Country Conference April 5, 2013 |

| "You have to Destroy the Maastricht Treaty to Save It" Posted: 27 Mar 2013 01:18 PM PDT There are plenty of news headlines rattling Europe today. Let's take a look at some of them. Severe Capital Controls in Cyprus In spite of the fact the Maastricht Treaty under which the eurozone was formed mandates a free flow of capital, Cyprus unveils severe capital controls. " Cyprus is the first eurozone country ever to apply capital controls, with limits on credit card transactions, money transfers abroad and the cashing of cheques. Depositors will be limited to credit card transactions of up to €5,000 per month and will be able take a maximum of €3,000 of bank notes out of the country per trip." Capital controls are said to expire in seven days. So, don't worry, its only temporary. Hopefully everyone understands the implied theory: " You have to Destroy the Maastricht Treaty to Save It." Top Orwellian Comments Of All Times - An American major after the destruction of the Vietnamese Village Ben Tre: "It became necessary to destroy the village in order to save it."

- Vice President Joe Biden: "We Have to Go Spend Money to Keep From Going Bankrupt."

- President George W. Bush: "I've abandoned free-market principles to save the free-market system."(For a discussion please see The Most Redeeming Feature of Capitalism is Failure)

- Nancy Pelosi said "We have to pass the health care bill to see what's in it." (YouTube Video)

- Larry Summers says "The central irony of financial crisis is that while it is caused by too much confidence, too much borrowing and lending and too much spending, it can only be resolved with more confidence, more borrowing and lending, and more spending." (Reuters)

But What about those advertised losses of 30% on large Cyprus depositors? Glad you asked. " Laiki depositors holding more than €100,000 may lose up to 80 per cent of their funds, and only get the remaining 20 per cent back over a period of years, Cyprus's finance minister said on Tuesday." Italy Industrial Orders Sink Dow Jones reports Italy Industrial Orders Fall in Jan on Declining Internal Demand " Italian industrial orders dropped for the third consecutive month in January and were down compared with the same period a year ago, hit by declining internal demand, the national statistics institute reported Wednesday. Orders fell 1.4% in January from December in seasonally-adjusted terms and were down 3.3% from January 2012 in unadjusted terms, Istat reported." Merkel Ally Backs Double-Digit Hike in Top Tax Rate If you thought Merkel and her CDU party were true conservatives, it's time for you to think again. Reuters reports Merkel CDU Ally Backs Double-Digit Hike in Top Tax Rate. " A senior conservative ally of Chancellor Angela Merkel, Annegret Kramp-Karrenbauer, premier of the western state of Saarland and a senior figure in the Christian Democratic Union (CDU), said in a weekend radio interview that Merkel's predecessor Gerhard Schroeder had gone too far by reducing the top rate to 42 percent from 53 percent in the 1990s." Is Poland Having Second Thoughts? The Financial Times reports Poland opens way to euro referendum. " Donald Tusk, Poland's prime minister, took a big political gamble on Tuesday when he opened the door to a referendum on joining the euro, in the face of strong public opposition to the common currency. The latest opinion survey shows 62 per cent of Poles are opposed to joining, with scepticism increasing markedly since the financial and debt crises hit Europe five years ago. But now Mr Tusk has publicly raised the possibility of allowing a referendum – demanded by rightwing opposition parties opposed to euro membership – in return for an agreement with the opposition to push through the necessary constitutional changes." Tusk is setting a trap. Tusk wants the constitutional changes now, but will only hold a vote when favorable. Should the vote fail, rest assured there will be another and another and another. Unless of course the eurozone splinters to high heavens in the meantime which of course is a likely possibility. The correct move is for the opposition to demand a referendum immediately, and if and only if it passes (it won't), should the constitutional changes be taken up. French Unemployment Hits 16-Year High President Francois Hollande's socialist policies are firing on all four cylinders now, except in reverse as French Unemployment Hits 16-Year High. The Financial Times reports " French unemployment nudged a record level in February as the jobless total rose for the 22nd month in succession to a 16-year high, adding to the acute political pressure on President François Hollande as he battles a stalled economy. The OECD predicts unemployment will reach 11.25 per cent, surpassing the record level of 10.8 per cent previously hit in 1994 and 1997." Except for Spain, Germany, Greece, Cyprus, Portugal, Italy, Ireland, Slovenia, Luxembourg, France, and various other eurozone countries, everything in the eurozone is quite lovely. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Bersani Pleads for "More Insanity" as Italian Government Talks Collapse Posted: 27 Mar 2013 10:14 AM PDT Pier Luigi Bersani, who heads the centre-left (Common Good) coalition has a mandate by the Italian president (Giorgio Napolitano), to form the next government of Italy and become its next Prime Minister. However, talks between Bersani, and Silvio Berlusconi's centre-right Popolo della Libertà PDL (the People of Freedom) alliance fizzled yesterday, as expected. Talks between Bersani and Beppe Grillo's Five Star Movement M5S fizzled today, also as expected. The reaction of Bersani as reported by the Financial Times is rather amusing. "Only an insane person can have the eagerness to form a government in this moment," declared Mr Bersani, grim faced and looking somewhat exasperated, at his webcast meeting with the Five Star Movement. "I am ready to take on this enormous responsibility and I would ask everyone to take on a little bit of it." The PDL offered to form a "Grand Coalition" with Bersani but only on grounds the centre-left cannot accept. Next up, president Napolitano is expected to seek a technocrat prime minister but odds the center-left, center-right, and M5S agree to that are essentially zero. Napolitani is the outgoing president and cannot call for new elections. His seven-year term ends May 15. The next head of state would then call for fresh elections. This is all playing out exactly as outlined on March 7 in What's Next for Italy? No Working Government for 7 Months, Then Elections in September. A tip of the hat to reader "AC" who made hung-parliament call before the February elections (see European Reader Offers Insights on Upcoming Italian Election on February 19, 2013). Explaining the Plea for More Insanity Bersani will not win again next time. Both M5S and PDL have surged in the polls taking votes away from the center-left. Bersani is not even expected to be the next center-left candidate in new elections. Rather, Matteo Renzi, Mayor of Florence is widely expected to be the next center-left party leader. So, this is Bersani's only shot, which explains his plea for more insanity. Bersani will be out. But to who? Don't rule out another hung parliament. The last election was a hung parliament between PDL and Bersani's centre-left. If Beppe Grillo's M5S wins the lower parliament in the next election, the result may very well be a hung parliament between PDL and M5S. Won't that be fun? Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Unwilling to Work; 25% in Hale County AL Collect Disability, 14 Million Nationwide; A Simple Solution Posted: 27 Mar 2013 12:57 AM PDT A NPR report " Unfit For Work" notes the startling rise in those on disability. Here are some interesting facts from the article. - Every month 14 million Americans receive a disability check.

- In 1961 the leading cause of disability was heart disease and strokes, totaling 25.7% of cases. Back pain was 8.3% of cases.

- In 2011 the leading cause of disability was a hard to disprove back pain, totaling 33.8% of cases. The second leading cause was an equally difficult to disprove "mental illness" at 19.2%. Strokes and heart disease fell to 10.6%.

- In West Virginia, a whopping 9% of the population collects disability checks. In Arkansas, 8.2% are on disability, and in Alabama and Kentucky, 8.1% collect disability. In Alaska, Hawaii, and Utah, the figure is 2.9%.

- In Hale County Alabama 1 in 4 receive disability checks.

- One thing nearly every case in Hale County Alabama has in common is Dr. Perry Timberlake who defines disability in a rather creative way.

- Those on Supplemental Security Income, a program for children and adults who are both poor and disabled is nearly seven times larger than 30 years ago.

- Once people go onto disability, they almost never go back to work. Fewer than 1 percent of those who were on the federal program for disabled workers at the beginning of 2011 have returned to the workforce.

Percentage of Population On Disability by State  click on chart for sharper image Children on Disability click on chart for sharper image Children on Disability  How Easy is it to Get Disability? How Easy is it to Get Disability? Hale county's Dr. Timberlake asks a simple question to all his patients. "What grade did you finish?" If you claim "back pain" and do not have a degree, Timberlake believes you are disabled. The Disability Deal Getting disability seems easy enough in some states, and especially easy in Hale County Alabama. But is disability better than minimum wage? The answer is yes. NPR author Chana Joffe-Walt explains: People who leave the workforce and go on disability qualify for Medicare, the government health care program that also covers the elderly. They also get disability payments from the government of about $13,000 a year. This isn't great. But if your alternative is a minimum wage job that will pay you at most $15,000 a year, and probably does not include health insurance, disability may be a better option.

Going on disability means you will not work, you will not get a raise, you will not get whatever meaning people get from work. Going on disability means, assuming you rely only on those disability payments, you will be poor for the rest of your life. That's the deal. And it's a deal 14 million Americans have signed up for.

Disability has become a de facto welfare program for people without a lot of education or job skills. Parents Force Kids to Underachieve Joffe-Walt explains the special plight of kids. When you are an adult applying for disability you have to prove you cannot function in a "work-like setting." When you are a kid, a disability can be anything that prevents you from progressing in school.

Jahleel's mom wants him to do well in school. But her livelihood depends on Jahleel struggling in school. This tension only increases as kids get older. One mother told me her teenage son wanted to work, but she didn't want him to get a job because if he did, the family would lose its disability check.

Kids should be encouraged to go to school. Kids should want to do well in school. Parents should want their kids to do well in school. Kids should be confident their parents can provide for them regardless of how they do in school. Kids should become more and more independent as they grow older and hopefully be able to support themselves at around age 18.

The disability program stands in opposition to every one of these aims. Clinton Ends Welfare As We Know It In 1996 Bill Clinton signed a welfare reform act, that he proclaimed to be the "End of Welfare As We Know It". It was. People moved off welfare on to even easier to get disability programs. Part of Clinton's welfare reform plan pushed states to get people on welfare into jobs, partly by making states pay a much larger share of welfare costs. The incentive "worked" using the term loosely. Welfare rolls shrank but disability rolls soared. Welfare Costs States Money Disability Doesn't A person on welfare costs a state money. That same resident on disability doesn't cost the state a cent, because the federal government covers the entire bill for people on disability. So states can save money by shifting people from welfare to disability. And the Public Consulting Group is glad to help.

PCG is a private company that states pay to comb their welfare rolls and move as many people as possible onto disability. "What we're offering is to work to identify those folks who have the highest likelihood of meeting disability criteria," Pat Coakley, who runs PCG's Social Security Advocacy Management team, told me.

The company has an office in eastern Washington state that's basically a call center, full of headsetted women in cubicles who make calls all day long to potentially disabled Americans, trying to help them discover and document their disabilities:

"The high blood pressure, how long have you been taking medications for that?" one PCG employee asked over the phone the day I visited the company. "Can you think of anything else that's been bothering you and disabling you and preventing you from working?"

The PCG agents help the potentially disabled fill out the Social Security disability application over the phone. And by help, I mean the agents actually do the filling out.

There's a reason PCG goes to all this trouble. The company gets paid by the state every time it moves someone off of welfare and onto disability. In recent contract negotiations with Missouri, PCG asked for $2,300 per person. For Missouri, that's a deal -- every time someone goes on disability, it means Missouri no longer has to send them cash payments every month. For the nation as a whole, it means one more person added to the disability rolls. Disability Fraud Who is making the case for the other side? Who is defending the government's decision to deny disability? Nobody. And that in a nutshell explains soaring disability roles and massive fraud. Disability fraud also makes a joke out of reported unemployment numbers. If you have a disability, you are no longer in the workforce. Not in Labor Force With a Disability  I would love to show data pre-recession. Unfortunately, the data only goes back to mid-2008. We can see however, that nearly 23 million Americans are not in the labor force because of "disabilities". I suggest "fraud" is more like it. Curious BLS Numbers Here's the curious thing: 14 million collect disability, but the BLS says 22.726 million are not in the labor force (not working), because of disabilities. What are the other 8.726 million doing? Is the BLS inflating disability numbers making the unemployment rate absurdly low, or are states doing that poor a job getting people off welfare and on to federal government disability programs? Some of both? Regardless, we need to stop this madness. Simple Solution One easy way to eliminate some of the fraud would be to put someone in charge of making a case for the other side. No, we do not need new Federal programs. All we need do is " Un-end Welfare as We Know It". If states had any incentive to stop disability fraud, we would not have so much of it. Make states responsible for a large portion of disability claims just as they are for welfare, and the number of people collecting disability will collapse. I have written many times about disability fraud, its relation to the unemployment rate, and its relation to expiring unemployment benefits. Inquiring minds may wish to consider some Disability Fraud Examples. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Wine Country Conference I am hosting an economic conference on April 5 in Sonoma, California. Proceeds go to the Les Turner ALS Foundation (Lou Gehrig's Disease). Please see My Wife Joanne Has Passed Away; Stop and Smell the Lilacs for my association with the disease. To learn about the economic conference with world-class speakers including John Hussman, Michael Pettis, Jim Chanos, John Mauldin, Mike "Mish" Shedlock, Chris Martenson with guest moderator Lauren Lyster and other Special Guests, please visit Wine Country Conference April 5, 2013 |