Mish's Global Economic Trend Analysis |

- Apocalypse Illinois: IOUs Projected to Hit $10.5 Billion, $163 Billion Total Accumulated Liabilities

- China's Art of Propaganda: Future So Bright You Need Sunglasses Inside

- CME Fedwatch and Bloomberg Rate Hike Odds Still Wrong; Deflationary Bust Coming

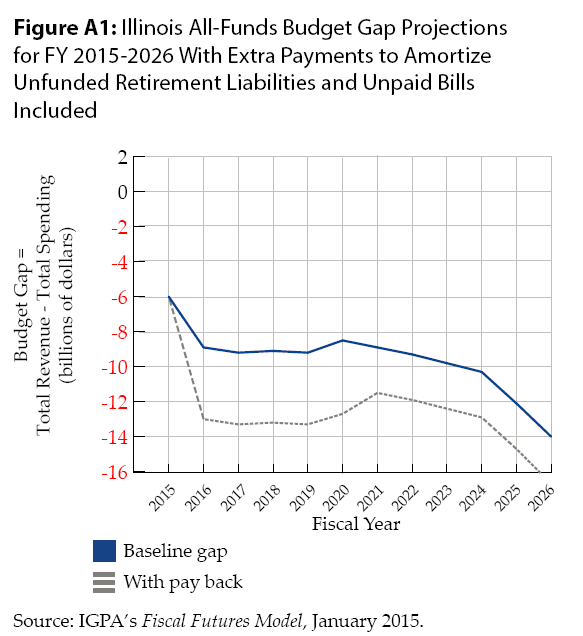

| Apocalypse Illinois: IOUs Projected to Hit $10.5 Billion, $163 Billion Total Accumulated Liabilities Posted: 11 Sep 2015 12:33 PM PDT Flat Out Broke Illinois is in serious fiscal trouble. Unpaid bills will hit about $10.5 billion later this year, counting unpaid lotto winners and state university bills. Lotto is a small problem overall, yet symbolic of the mess the state is in. Because Illinois has no current budget, the state does not pay lotto winners. Instead it sends the winners IOUs. Yesterday, two Illinois lottery winners filed a class action lawsuit over unpaid prizes. Promises, Promises Unpaid bills do not count additional promises that politicians seek. For example, Chicago Mayor Rahm Emanuel wants a half billion dollars from the state to shore up the Chicago school budget. Where is that supposed to come from? The list of "wants" is endless; the reality is "Illinois is flat out broke". When will multiple downgrades from Moody's, Fitch, and the S&P hit the overall state, not just the city of Chicago? Drowning in Red Ink In a big understatement of Illinois' problem, a Crain's Chicago headline reads Illinois IOUs Growing Fast, Could Pass $8.5 Billion by Yearend. Slowly but surely, Illinois government is beginning to drown in red ink, State Comptroller Leslie Munger said today, as the cost of the continuing Springfield budget war steadily worsens the already bad condition of state finances.Humorous Solution My favorite comment to Crain's article comes from "Earl" who sarcastically asks "Why not try not spending money the state does not have?" Indeed. Let's try that. Well, actually Illinois has been doing that for years. And bad as $10.5 billion sounds, it's but a small drop in the cumulative bucket. Apocalypse Illinois Drum roll please: In January, Illinois' total cumulative liability was $159 billion. Counting $4 billion in spending for state universities, lottery winners, etc., the total cumulative liability is on the order of $163 billion today, and growing more rapidly than ever. A study released this past January called "Apocalypse Now" discusses the "Consequences of Pay-Later Budgeting in Illinois". Accumulated Debts Per Capita The US Census Bureau reports the Illinois population is on the order of 13 million and growing slowly if at all. The accumulated bill amounts to $12,538 per every man, woman, and child. But children don't pay bills or taxes. So let's do the calculation based on the census estimate of 4,772,723 households. That accumulated bill amounts to $34,152 per household. Problem Understated I propose the Apocalypse Now study hugely understates Illinois problems. What About?

Sobering View I discussed point eight in detail on July 21 in SuperBull Club: RBC Ups Morgan Stanley, Says Bull Market to Continue 6 Years; Sobering Alternative View from GMO. Sobering Alternative View from GMOReforms, Not Tax Hikes Tax hikes are not the answer. Tax hikes will just cause more Illinois taxpayers and businesses to flee. Business exodus is already a serious problem. For details, please see Get Me the Hell Out of Here. Massive reforms are the only thing that can possibly save this state. Meanwhile, Debt downgrades from Moody's, Fitch, and the S&P are just around the bend, and deservedly so. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| China's Art of Propaganda: Future So Bright You Need Sunglasses Inside Posted: 11 Sep 2015 12:10 PM PDT The future of China is so bright you need to wear sunglasses inside to see. That's the essence of recent propaganda from China, where the state promotes good lies with discussion of the bad truth strictly forbidden. Please consider Don't Fret About the Data, China's GDP Forecast to be Good News. "The focus for the month of September will be strengthening economic propaganda and . . . promoting the discourse on China's bright economic future and the superiority of China's system," the party's propaganda department said in a directive to national media outlets.Say the right things and you move up the party line. Say the wrong things and you are put in prison or shot. China has no human rights, appalling property rights, illiquid bond markets of insufficient size, and a pegged currency it can no longer control smoothly. Capital controls round out the mess. Yet, people think the Yuan will "soon" become the world's reserve currency, replacing the US dollar. I have heard these yuan reserve currency "soon" stories for at least a decade. What a joke. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CME Fedwatch and Bloomberg Rate Hike Odds Still Wrong; Deflationary Bust Coming Posted: 11 Sep 2015 01:56 AM PDT As of September 10, the CME has the odds of a September hike by the Fed at 24%. Bloomberg says the probability of a move is 28%. Bloomberg Rate Hike Odds  CME Fedwatch Odds  Both Models Wrong What's wrong with both models is they still presume a quarter point hike. Neither Bloomberg nor the CME allows for the possibility of a Fed hike to precisely 0.25% or to a smaller tighter range. Given the effective Fed Funds Rate is 0.14% (see upper right of Bloomberg chart), resetting the rate to a flat 0.25% from the current range of 0.00-0.25% (now at 0.14%), would be both a "move" and a "hike". Tighter Range The Fed could also use ranges as Bloomberg and CME imply, but target ranges in 1/8 of a point increments rather than 1/4 point increments. For example the Fed could target a range of 0.25% to 0.375%. I suspect the odds of a move to a flat 0.25 or a range (0.25% to 0.375%), are far greater than Bloomberg's "probability of a move" set at a mere 28%. I went over this before, on August 19, in Plotting the Fed's Baby Step 1/8 Point Hikes; Yellen vs. Greenspan "Measured Pace". I updated my charts today. Flattening of Rate Hike Expectations  Using Fed fund futures from CME, I calculated implied interest rates through December 2017. The line in Blue shows what futures implied on August 19. The line in red is from September 10. Note the flattening of the curve. This has been happening pretty much all year. The market initially penned in hikes for January. The hikes then shifted to March, then June, then September, and now December by both the Bloomberg and CME models. Range Watch Curve Watchers Anonymous is closely watching the implied baby steps in the Fed fund futures. Incrementally, the hikes appear as follows.

Baby Steps Plotted Fed fund futures imply a very slow tightening of 3-6 basis points a month. The only exception is January to February of 2017 where the incremental rise is 8 basis points (0.080 percentage points). The Fed does not set policy every month. Instead it does so about eight times a year. FOMC dates are not yet set for 2017, but futures imply something like the following. Fed Rate Hike Expectations Through 2017  Yellen vs. Greenspan

Just Get On With It! Via email, Albert Edwards at Society General writes: The clamour for the Fed not to enact the long-awaited ¼% rate hike next week is growing by the day. Misgivings come not just from reputable mainstream commentators, but now also the World Bank has repeated the IMF's recent words of caution in advising delay. What a load of nonsense! My esteemed colleague Kit Juckes characterises the current consensus thinking as "If the Fed hikes, pestilence, plague and never-ending deflation will follow." Well even those like me who see a deflationary bust awaiting think the Fed should hike next week – because the longer you leave it, the bigger the financial market excesses become, and the bigger the risk of financial dislocation and global recession ensuing. Have we learned nothing from the 2008 Great Recession? Just get on with it!Exactly! A deflationary bust is coming and there is nothing the Fed or any central bankers can do about it. And when the bubble busts, Paul Krugman, Larry Summers, the World Bank, and Christine Lagarde at the IMF will all be singing the "I told you so" tune. The irony is Krugman, Summers, the World Bank and the IMF are all wrong. The seeds of the upcoming deflationary bust were planted, watered, and over-fertilized by central bankers everywhere, all in the asinine name of "price stability" and deflation fighting. For further discussion on the sheer ridiculousness of price stability policy, see Cross-Border Deflation: US Export Prices Collapse Most Since July 2009; How Damaging is Price Deflation? Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment