Mish's Global Economic Trend Analysis |

- Fed Apologist Ritholtz Interviews Fed Apologist McCulley

- Investigating Consumer Confidence: 3-Month Low? 10-Month Low? Near Record High?

- ISM Weaker Than Expected, Details Weak, Exports Contract Third Month

- China PMI Contracts Fastest Since February-March 2009

| Fed Apologist Ritholtz Interviews Fed Apologist McCulley Posted: 01 Sep 2015 10:17 PM PDT Bloomberg columnist Barry Ritholtz interviewed Paul McCulley, former chief economist at PIMCO, and often mentioned FOMC candidate on the Fed's performance. The Podcast is over two hours long, so let's just go with Ritholtz's brief summary: McCulley Demands Apology on Behalf of the Fed. McCulley noted those who claimed QE and ZIRP were going to cause inflation and the collapse of the dollar were totally wrong, and he demanded these critics of the Federal Reserve owe former Ben Bernanke an apology. Had the Fed Chief listened to them, we would have found ourselves in a modern day depression.Rebuttal In a blend of a monetarist and Keynesian thinking, McCulley supports Fed policies of QE and is "especially harsh on the Austerians, whom he said made the recovery weaker than it need be by thwarting traditional Keynesian stimulus." For starters, I dispute the notion that without QE and intervention that "we would have found ourselves in a modern day depression" as Ritholtz maintains. Ritholtz's claim is a poorly-formed hypothesis presented as fact. Yes, it's true that many in the Austrian camp predicted a dollar crash and high inflation. But I am in the Austrian camp camp and debt deflation has been my model, and still is my model. As for an apology, what about an apology from the Fed for blowing serial bubble after bubble of increasing amplitude? It's inane to demand an apology from those who warned in advance, and correctly so, of the housing bubble and subsequent crash. In a twist of irony, McCulley gloats over the alleged lack of inflation, but it's pretty clear he has his blinders on as to what inflation is and ways it can be spotted. In the case of Fed policy, inflation did not manifest itself in the CPI, but rather in asset bubbles, again and again. Challenge to Keynesians Only Keynesian and Monetarist fools (there is no more polite word), believe a low CPI is a big concern. I repeat my Challenge to Keynesians "Prove Rising Prices Provide an Overall Economic Benefit". Consumer Price Deflation NOT Damaging Even the BIS has concluded that routine consumer price deflation is no threat. For details, please see Historical Perspective on CPI Deflations: How Damaging are They? Income Inequality and Leverage China and the emerging markets are imploding right now. Leverage is as high as ever. Fed policy induced corporations to go into debt to buy back their own shares at absurd prices. Janet Yellen pisses and moans about income inequality, as does Ritholtz. Both are blind to the fact the Fed is the direct sponsor of it all. Unfounded Gloat This Keynesian gloat about the Fed saving the world is laughable because the final chapter has not been written. Assets are arguably as overpriced now as they were in 2000, and 2007. As with Japan, another lost decade in the US is likely. Demanding an apology on behalf of the Fed is like demanding an apology on behalf of a doctor who cuts off the wrong leg of a cancerous patient if the doctor gets it right the second time. It's the Fed that owes us all an apology. Barry, Paul, where the hell is that apology? But Keynesians and Monetarists don't apologize. They just demand more and more stimulus and debt in the inane belief the cure for a debt problem is more spending and more debt. The average 7th grader can easily see the fallacies of such nonsense. Unfortunately, as students progress through high school and college, repeated brainwashing by professors in academic wonderland about the alleged benefits of easy money has warped a lot of minds, in this case, the minds of the interviewer and the interviewee. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Investigating Consumer Confidence: 3-Month Low? 10-Month Low? Near Record High? Posted: 01 Sep 2015 11:05 AM PDT Last week, three different measures of consumer confidence came out:

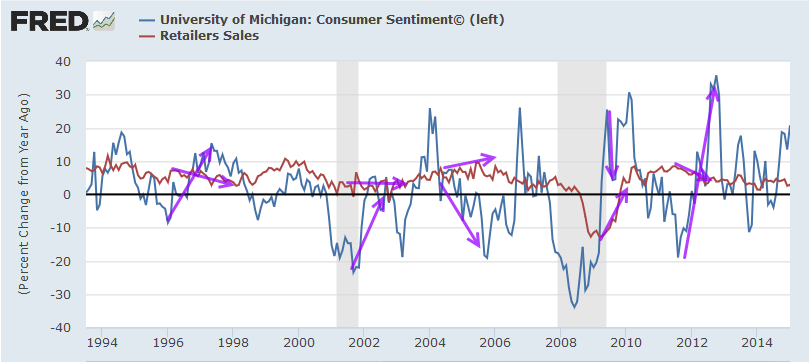

Claim of Importance Bloomberg states "Consumer sentiment is directly related to the strength of consumer spending." Let's investigate that claim starting with a look at the latest results from each survey. Consumer Confidence On August 25, the Conference Board's "Consumer Confidence Level" soared well ahead of any Bloomberg Consensus estimate with a reading Bloomberg stated "will have forecasters scratching their heads." Enormous improvement in the assessment of the current labor market drove the consumer confidence index well beyond expectations, to 101.5 in August for a more than 10 point surge from July. A rare 6.5 percentage point drop to 21.9 percent in those describing jobs as currently hard to get points to outsized gains for the August employment report. This reading will have forecasters scratching their heads. The gain for this reading lifts the present situation component to 115.1 for a more than 11 point increase from July that points to consumer power for August.Head-Scratching Sentiment Three days later, the University of Michigan release was another head-scratching event. Bloomberg reported Consumer Sentiment in U.S. Declines to a Three-Month Low. The University of Michigan sentiment number came in at 91.9, well below any guess in Bloomberg's Consensus Estimate Range of 92.7 to 95.0. An early reading on the effect of global volatility is downbeat as the consumer sentiment index came in well below expectations, at 91.9 for the final August reading. The mid-month reading was 92.9 which roughly implies a pace near 91.0 over the last two weeks which is the softest since May.Consumer Sentiment  Belief vs. Reality In regards to consumer confidence, Bloomberg stated "The Yellen Fed has put great emphasis on the importance on consumer confidence readings and this report points to job-driven strength ahead for household spending." Let's compare Yellen's belief to reality. Bloomberg conveniently provided this chart.  Here's a chart I put together last month on sentiment and sales. University of Michigan Sentiment vs. Sales  To be fair, one needs to look at per capita spending and factor in boomer dynamics such as aging, etc. However, I do not have access to the conference board data, and the University of Michigan data on Fred is out of date. Let's consider one more measure of sentiment. Gallup Economic Confidence Index On July 28, Gallup reported U.S. Economic Confidence Index Continues Downward, at -14. Gallup's Economic Confidence Index continued its gradual, downward slide, reaching -14 for the week ending July 26. This represents a 10-month low for the index.Gallup Economic Confidence  Polling Methods

Questions

Poll Comparison

The surveys are so out of line with each other, it is impossible that "sentiment" matches spending, no matter how one adjusts the data. In fact, the above charts are so screwy that one might wonder if it's possible to accurately measure sentiment at all. Assuming sentiment can be measured (and we have three different surveys that purportedly do just that), the usefulness of such wildly differing surveys is not readily apparent. Yellen can believe what she wants, but faith in sentiment as a leading indicator or purveyor of future economic spending patterns is seriously questionable, at best. Forced to select a single survey, I would go with a phone survey over a paper survey, and a large sample size over a smaller one - Gallup. By the way, the University of Michigan and Gallup surveys are at least going the same direction this year. The Conference Board survey is the odd man out. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ISM Weaker Than Expected, Details Weak, Exports Contract Third Month Posted: 01 Sep 2015 09:42 AM PDT Those expecting a boost from the ISM report for August were disappointed today. The Bloomberg Consensus estimate for ISM was 52.8, with a range of 51.5 to 54.0. The report was below any economist's expectation at 51.1. The ISM index, at a lower-than-expected 51.1, is signaling the slowest rate of growth for the factory sector since May 2013. And the key details are uniformly weak.ISM Details Let's investigate all the details of today's report straight from the Institute for Supply Management Manufacturing ISM® Report On Business® released this morning.

Key Points

There's nothing in the ISM report to make the Fed want to hike, but the Fed will do what they want. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| China PMI Contracts Fastest Since February-March 2009 Posted: 01 Sep 2015 02:39 AM PDT China manufacturing and services are both in contraction at the fastest rate since early 2009. The Caixin China General Manufacturing PMI shows operating conditions deteriorate at fastest rate since March 2009. Chinese manufacturers saw the quickest deterioration in operating conditions for over six years in August, according to latest business survey data. Total new orders and new export business both declined at sharper rates than in July, and contributed to the most marked contraction of output since November 2011. Lower production requirements prompted companies to reduce their purchasing activity at the fastest rate since March 2009, while weaker client demand led to the first rise in stocks of finished goods in six months. Meanwhile, softer demand conditions contributed to marked falls in both input costs and output charges in August.Key Points

China Manufacturing PMI  Composite Contracts Most Since February 2009 The bad news in China does not stop with manufacturing. Markit reports the Caixin China General Services PMI has the fastest contraction of output seen since February 2009. Key points

By now it should be perfectly clear to everyone that the entire global economy is cooling and the US will not decouple from that slowdown. Nonetheless, most economists, including those at the Fed, still do not see the obvious. Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment