| War in Ukraine - Latest Maps - Cauldron Closed Posted: 10 Feb 2015 12:34 PM PST In my search for the latest military maps in Ukraine I came across this LiveUAMap purportedly from February 10.  Compare the above map with the following map posted by Colonel Cassad today.  The map above, just shows the cauldron (surrounded forces not all surrounding separatist held territory). Mentally line up the intersection of M103 and M104 with the same intersection in the first map.Cauldron ClosedYesterday Jacob Dreizin pinged me with this comment ... Hello Mish

Former rebel leader Strelkov's social media page is quoting the DNR Ministry of Defense and (separately) Strelkov himself as stating that the Debaltsevo-Artemovsk road has been cut off. In other words, the lid on the cauldron has finally shut.

This is generally a credible site, if you ignore the occasional crazy rumors being passed around and just focus on the overall direction of the fighting.

Other posts on this site suggest that Novorossia forces are now digging in along the road, to prevent reinforcements or supplies coming into the cauldron. They are also claiming deep LNR forays into Debaltsevo itself.

It's quite likely that Colonel Cassad will confirm in one of his longer posts later today. Cassad is renowned for detail and analysis, but not for breaking news.

Please note, the term "cauldron" now refers to the (now-shrunken) lower half of the Kiev-held salient as per the maps you've shown. There is still a gap at the "top" that the DNR/LNR were unable to close.

I must say, the degree of Ukrainian command and coordination incompetence is stunning. Kiev's forces were repeatedly taken by surprise by the direction and scope of DNR/LNR moves to shrink and cut off the salient. Reserves were also not brought to bear in time, if at all.

It's clear to me that the DNR/LNR's Russian advisors have again outwitted Kiev's U.S. advisors.

Jacob Colonel Cassad February 10The second map above was posted by Colonel Cassad today (map dated yesterday), in his post Debaltsevsky Boiler. The Debaltsevsky [Debaltsevo] group is split into two parts. 5,000 are trapped in the rear boiler [cauldron].

The main problem of the junta [Ukrainian forces] is the rapid exhaustion of resources including serious problems with fuel and ammunition for heavy weapons. Yesterday the Ukraine forces retreated 4 kilometers in the Chernukhin area. Further collapse of the boiler is inevitable. In a Q&A portion following Cassad's article, Schneider Krieg (who also has his own "live" journal), pinged Cassad with his post on the " North Boiler". Cassad responded with " It depends on how much they pulled out of the boiler before the lid slammed shut. I quite agree with you, there can not be less than 4 thousand and probably closer to 5." MariupolIn regards to Mariupol, Cassad says ... A counteroffensive junta operation near Mariupol is more of a rather loud publicity stunt than a serious blow. The junta moved through neytralku and a series of empty settlements, but in practice there were no serious attacks of the main line of defense. The reason for this attack is pending decisions of the Minsk summit. The junta is trying in the remaining time to seize control of any bit of territory they can get. Word Regarding Translation Translation of these articles is difficult. About a week or so ago I reported the cauldron had closed when Cassad was actually giving his opinion that it would close. The cauldron or " boiling pot" as Cassad calls it, has indeed closed for certain as of yesterday. There are about 5,000 trapped in the rear cauldron of which 1,000 to 1,500 are support personnel. Meanwhile, Kiev denies any troops are trapped. Nothing coming from Kiev on the war is believable. Translation Correction:Jacob Dreizin informs me there are 5,000 trapped in the lower cauldron of which 1,000 to 1,500 are support personnel. I originally stated 1,000 to 1,500 were trapped in the lower cauldron. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Cold Water, Frosty Relations, Wildly Misleading Claims; Time Ticking Away in Greece; Calendar of Events Posted: 10 Feb 2015 10:20 AM PST From Frost to Cold WaterEquity markets cling to hopes of agreement with Greece, rhetoric from Germany is anything but encouraging. Yesterday, the Financial Times reported Merkel Frosty on Greece's Bailout Plans. Today the same story appears with the title of Merkel Pours Cold Water on Greece's Push to End Bailout. Chancellor Angela Merkel poured cold water on a push by Greece's new government to end its bailout and strike a new financing deal with its creditors, saying the current programme was "the basis of any discussions that we have".

Earlier in the day, Germany's powerful finance minister hinted darkly that a Greek plan to leave the bailout at the end of the month could draw a harsh reaction from financial markets.

"I wouldn't know how financial markets will handle it, without a programme — but maybe he knows better," Wolfgang Schäuble told reporters, referring to Alexis Tsipras, the new Greek premier. Cold Water, the Theme of the WeekCold water appears to be the theme of the week. Bloomberg reports German Finance Minister Schaeuble Just Poured Cold Water on Market Expectations for a Greece DealGreece offered compromises ahead of an emergency meeting with its official creditors tomorrow as German Chancellor Angela Merkel remained unyielding over terms of the country's bailout conditions.

Greek Finance Minister Yanis Varoufakis told lawmakers on Monday that the government intends to neither tear up the existing bailout agreement, nor allow the budget to be derailed. He said Greece will implement about 70 percent of reforms already included in the current bailout accord.

The European Commission denied reports it will present a compromise proposal at the meeting tomorrow, saying "very intense contacts are ongoing between" Commission President Jean-Claude Juncker, Prime Minister Tsipras and others, and that the plan being worked on is to keep Greece in the euro area. Expectations are "low" for a final pact this week, the commission said.

Greece sought to drum up support for a 10 billion-euro ($11.3 billion) bridge plan ahead of the euro-area finance ministers' meeting in Brussels on Wednesday. The country is seeking to stave off a funding crunch, while also buying time to push creditors to ease some austerity demands.

German political leaders have said they will not extend more assistance to Greece without strings attached. Merkel said in Washington on Monday that the existing aid programs are the basis for Greek talks.

"I'm waiting for Greece to come forward with a viable recommendation and then we'll talk about it," she said. The only " viable recommendation" from Greece that Germany seems willing to accept is 100% of what Germany wants. Wildly Misleading ClaimsToday, Euro Insight reports EU-Greek Relations Soured by Leaks; Sides Further Apart. Brussels officials 'infuriated' by 'wildly misleading' Greek claims that Juncker and U.S. Treasury are backing Syriza plan to alleviate debt; EU official says Greeks are 'digging their own graves;'

The carefully orchestrated dance between the new Greek government and its European creditors appeared to crack Tuesday, with top Brussels officials infuriated by what they see as wildly misleading claims coming from Athens.

A senior European official, who spoke on condition of anonymity, described the situation as "berserk" and said, "there is no plan."

He added that the European Commission and U.S. Treasury were both perturbed at the way they had apparently been represented externally by Greek officials. A team from the U.S. Treasury led by Daleep Singh, deputy assistant secretary for Europe & Eurasia, was in Athens late last week.

"The Greeks are digging their own graves," the EU official said.

Early Tuesday, Greece floated its latest funding plan via press leaks, including to the Kathimerini newspaper, proposing a bridge financing programme that would lead to a "new deal" with creditors from September onwards.

There were reportedly four parts to the new deal: 30% of the existing memorandum with the Troika will be cancelled and replaced with 10 new reforms agreed with the OECD; Greece's primary surplus target would be cut from 3% of GDP this year to 1.49%; Greek debt would be reduced via an already announced swap plan; and the "humanitarian crisis" would be alleviated via policies announced by Prime Minister Alexis Tsipras Sunday.

The first official described the plan as "hopeless" and added, "how can you have a plan when you make no payment obligation till the autumn and then you probably scrap that." Time Ticking Away- February 11 Emergency meeting of the eurogroup, the committee of 19 eurozone finance ministers, to kick-start negotiations over a possible new bailout for Greece.

- February 12 EU summit in Brussels, the first attended by Greek PM Alexis Tsipras, who is expected to meet German chancellor Angela Merkel on the sidelines.

- February 16 Regularly scheduled eurogroup meeting which ministers have said is the deadline to agree an extension of the EU's bailout programme, which Mr Tsipras has already rejected.

- February 28 Eurozone bailout programme ends. Without an extension, Athens will not receive final aid tranche of €1.8bn.

- March €1.4bn payment due on IMF loan and around €1bn to other creditors.

The first critical date would appear to be February 16, the date by which Greece needs to agree to the bailout program. However, that's an unofficial date. Numerous countries need to vote on the extension even if Greece agrees to kiss Germany's feet. From a practical standpoint, if Greece agrees to demands by the 28th, eurozone leaders will find a way to make it happen. At this point a deal seems unlikely. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

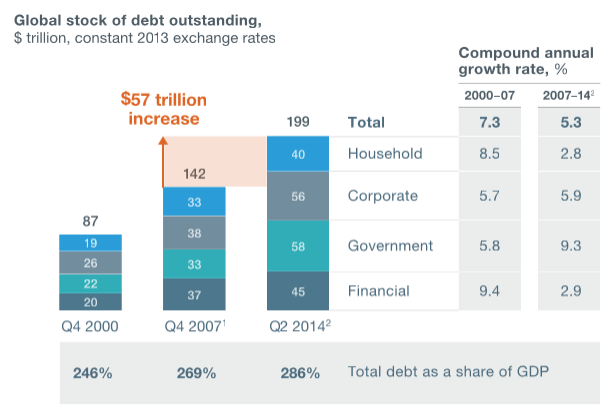

| Seven Years Later, Global Debt Keeps Piling Up, $57 Trillion More Than 2007 Posted: 10 Feb 2015 01:12 AM PST Central bankers still have not figured out the absurdity of their efforts to cure deflation via low interest rates. By forcing down interest rates and encouraging more lending, debts of all sorts keep piling up with no realistic way of paying those debts off. Debt and (Not Much) DeleveragingInquiring minds are digging into a fascinating albeit lengthy (256 page) McKinsey study of debt and deleveraging since the great financial crisis seven years ago: Debt and (Not Much) DeleveragingSeven years after the bursting of a global credit bubble resulted in the worst financial crisis since the Great Depression, debt continues to grow. In fact, rather than reducing indebtedness, or deleveraging, all major economies today have higher levels of borrowing relative to GDP than they did in 2007. Global debt in these years has grown by $57 trillion, raising the ratio of debt to GDP by 17 percentage points. That poses new risks to financial stability and may undermine global economic growth.

Government Debt

Government debt is unsustainably high in some countries. Since 2007, government debt has grown by $25 trillion. It will continue to rise in many countries, given current economic fundamentals. Some of this debt, incurred with the encouragement of world leaders to finance bailouts and stimulus programs, stems from the crisis. Debt also rose as a result of the recession and the weak recovery. For six of the most highly indebted countries, starting the process of deleveraging would require implausibly large increases in real-GDP growth or extremely deep fiscal adjustments.

Household Debt

Household debt is reaching new peaks. Only in the core crisis countries—Ireland, Spain, the United Kingdom, and the United States—have households deleveraged. In many others, household debt-to-income ratios have continued to rise. They exceed the peak levels in the crisis countries before 2008 in some cases, including such advanced economies as Australia, Canada, Denmark, Sweden, and the Netherlands, as well as Malaysia, South Korea, and Thailand. These countries want to avoid property-related debt crises like those of 2008.

China

China's debt has quadrupled since 2007. Fueled by real estate and shadow banking, China's total debt has nearly quadrupled, rising to $28 trillion by mid-2014, from $7 trillion in 2007. At 282 percent of GDP, China's debt as a share of GDP, while manageable, is larger than that of the United States or Germany. Three developments are potentially worrisome: half of all loans are linked, directly or indirectly, to China's overheated real-estate market; unregulated shadow banking accounts for nearly half of new lending; and the debt of many local governments is probably unsustainable. However, MGI calculates that China's government has the capacity to bail out the financial sector should a property-related debt crisis develop. The challenge will be to contain future debt increases and reduce the risks of such a crisis, without putting the brakes on economic growth.

The rapid growth of shadow banking in China is a second area of concern: loans by shadow banking entities total $6.5 trillion and account for 30 percent of China's outstanding debt (excluding the financial sector) and half of new lending. Most of the loans are for the property sector. The main vehicles in shadow banking include trust accounts, which promise wealthy investors high returns; wealth management products marketed to retail customers; entrusted loans made by companies to one another; and an array of financing companies, microcredit institutions, and informal lenders. Both trust accounts and wealth management products are often marketed by banks, creating a false impression that they are guaranteed. The underwriting standards and risk management employed by managers of these funds are also unclear. Entrusted loans involve lending between companies, creating the potential for a ripple of defaults in the event that one company fails. The level of risk of shadow banking in China could soon be tested by the slowdown in the property sector.

What Happened to Deleveraging?

Growing government debt has offset private-sector deleveraging in advanced economies Rising government debt (debt of central and local governments, not state-owned enterprises) has been a significant cause of rising global debt since 2007. Government debt grew by $25 trillion between 2007 and mid-2014, with $19 trillion of that in advanced economies. To be sure, the growth in government spending and debt during the depths of the recession was a welcome policy response. At their first meeting in Washington in November 2008, the G20 nations collectively urged policy makers to use fiscal stimulus to boost growth.

Not surprisingly, the rise in government debt, as a share of GDP, has been steepest in countries that faced the most severe recessions: Ireland, Spain, Portugal, and the United Kingdom. The challenge for these countries now is to find ways to reduce very high levels of debt.

Given current primary fiscal balances, interest rates, inflation, and projected real GDP

growth rates over the next five years, we calculate that the ratio of government debt to GDP will continue to grow in many advanced economies, including Japan, the United States, the United Kingdom, and a range of European countries.

Mortgage Debt

Real estate and land prices are the major drivers of household debt over time What is causing the continuous rise of household debt around the world? Rising mortgage debt is the main cause, as documented in research by Jordà et al.36 In the United States, for example, household debt grew from just 16 percent of disposable income in 1945 to 125 percent at the peak in 2007, with mortgage debt accounting for 78 percent of the growth (Exhibit 15). Mortgage debt represents the majority of household debt growth in other countries as well. Our data show that mortgages now account for 74 percent of household debt in advanced economies and 43 percent of household debt in developing economies (where household loans also include borrowing for small family businesses).

Revisit Tax Incentives for Debt

Because real estate and credit bubbles helped trigger the 2008 financial crisis and many previous crises, policy makers should reconsider the tax preferences given for household mortgages. The incentives that governments give for real estate vary widely across countries, but include deductibility of mortgage interest expenses and preferential capital gains treatment on residential home sales.

While these incentives are usually adopted to promote the social goal of homeownership, in practice they provide the greatest benefits for high-income households that pay the highest taxes. Moreover, they help create housing bubbles by encouraging households to take on larger mortgages to buy more expensive homes.

Policymakers therefore may need to revisit the mix of incentives given for homeownership and balance this goal against public incentives for other investments – particularly those that expand the long-term productive capacity of the economy, which residential real estate in most cases does not. Kill Incentives - All of ThemThere is much more in the report, some of which I agree with, but some not. For example, I agree with McKinsey in regards to mortgage incentives and housing bubbles, but why stop there? I suggest that government planners should stay out of the incentive business altogether and instead let the free market work as it will do if left alone. Sowing Inflation, Reaping Deflation Central banks in general are hell-bent on forcing more debt into the system. Given that debt (and the ability to pay it back) is precisely the problem, attempts to force more debt into the system is 100% guaranteed to blow up at some point. Asset bubbles are building and the Fed (central bankers) don't see them. Instead, they focus on consumer price deflation which actually should be a welcome thing. This theme was a recent topic of mine. In case you missed it, please see Sowing Inflation, Reaping DeflationMike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

No comments:

Post a Comment