Mish's Global Economic Trend Analysis |

- 4th Quarter GDPNow Forecast Sinks to +0.6 Percent; Fed Futures Target 1 Hike in 2016; Disastrous Data Recap

- More Fed Confessionals; Funny Oil Videos; In Search of Bullard; Inflation Expectations

- Manufacturing Inventories Decline But Inventory-to-Sales Ratio Doesn't Budge; Another Recessionary Looking Chart

- Producer Prices Decline More Than Expected, Services Disappoint; Oil Approaches $29

- Industrial Production Numbers and Revisions Shockingly Bad; Autos Have Peaked

- Empire State Manufacturing Index Posts Horrific -19.37, Lowest Reading Since April 2009

- December Retail Sales Negative; Other Economic Data Horrid

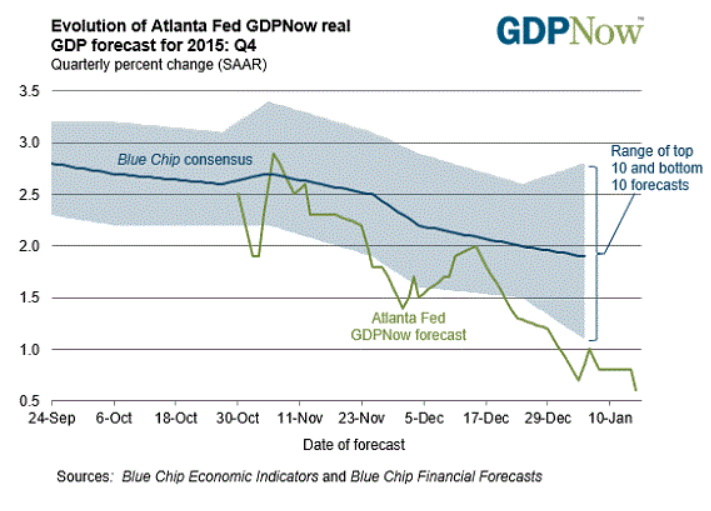

| Posted: 15 Jan 2016 03:30 PM PST I have never seen the Atlanta Fed take as long to post a scheduled update to their GDP Forecast as they did today. Their forecast came out late this afternoon, but it did beat the market close.  Latest forecast — January 15, 2016 The GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2015 is 0.6 percent on January 15, down from 0.8 percent on January 8. The forecast for fourth quarter real consumer spending growth fell from 2.0 percent to 1.7 percent after this morning's retail sales report from the U.S. Census Bureau and the industrial production release from the Federal Reserve. 5 Disastrous Economic Reports From Today

That's likely the worst set of economic reports since the last recession. Fed Futures Target 1 Hike in 2016 Following today's set of horrific reports, odds of rate hikes in 2016 dropped substantially. Fed Fund Futures analysis show the March hike odds shrank all the way to 31% from 55% last month.  The first hike is now expected in July, but barely. And looking all the way out to December, the futures still suggest only one hike.  Note the significant 33.9% chance of no more hikes for the entire year! Nonetheless, a parade of Fed governors attempted to talk up the strength of the economy over the past few days, even today. The market laughed in their face. Mike "Mish" Shedlock |

| More Fed Confessionals; Funny Oil Videos; In Search of Bullard; Inflation Expectations Posted: 15 Jan 2016 12:48 PM PST Another Fed Confessional In reference to statements made by Fed officials that the decline in the price of oil was good for the economy, San Francisco Fed president John Williams now admits "We Got It Wrong". Click on the link for a video submitted by Zero Hedge on January 10. On January 9, Forex Live provided some quotes ... The Fed's Williams was asked about the impact of oil on the US economy. "The Fed got it wrong when it predicted a drop in oil prices would be a big boon for the economy," he said. "It turned out the world had changed; the US has a lot of jobs connected to the oil industry." More accurately, Williams said "We got this wrong". The above statements attributed to Williams are not quotes but they are a close paraphrase. I spent quite a while looking for "Fed got it wrong" before finding the above video. Forex Live also stated "At this time last year the Fed's Bullard was saying: The 'oil price drop is very unambiguously positive for US.'" In Search of Bullard I searched high and low but could find no such statement by Bullard. Purportedly that statement comes from a Bloomberg TV interview on January 30, 2015: Bullard Says Rates at Zero Not Right for U.S. Economy. I played the interview. Bullard made no such statement then, or at any other time, at least that I can find. Instead, you will find a mess of total nonsense about inflation expectations as well as some statements that are far more reasonable. Bullard did state normal interest rates are close to 4%. The video conclusion was interesting. Bloomberg: How confident are you in your forecasts given all the cross-currents out there? Bullard: Very confident. (laughing). I think forecasting is always a hazardous thing. I think one of the things is you always have to keep in mind is, no matter who you are, you put out a forecast and you know you're gonna be wrong, because that's the way the macro economy works. And you have to learn, which direction were we wrong, and how should we shade our forecast next time to try to accommodate that. And that's the best you can do because it's a wild bucking bronco to try to forecast the US economy. Bloomberg: You hope to be less wrong when you put out these forecasts. Bullard: Yes, less wrong. Better Idea Instead of attempting to ride a "wild bucking bronco" with predictions known in advance to be wrong, why should the Fed forecast at all? Why not let the market sort this out instead of a bunch of purported wizards who essentially admit they don't know what they are doing? Could a free market in interest rates possibly have done worse than the dotcom bubble, followed by the housing bubble, followed by the equity and junk bond bubbles we are in now? Funny Oil Videos The statement attributed to Bullard may or may not have been made by Bullard, but Larry Kudlow did make that exact statement. In a CNBC video in November of 2104, Kudlow stated emphatically Drop in Oil Prices is Unambiguously Good. Here is a second Kudlow interview discussing oil. Both videos are downright funny in retrospect. Crude Weekly Chart  Inflation Expectations Inquiring minds may be asking "What about those inflation expectations?" Fear not, I just happen to have the answer from yesterday: Bullard Warns on Weak Inflation Expectations.  By the way, I left out a key snip from the Bloomberg-Bullard interview from last year. On January 30, 2015, Jim Bullard said "I would expect them [inflation expectations] to gradually come back up. We'll see. If that doesn't happen, then I would start to get very concerned that our credibility was eroding and markets were starting to doubt our ability to hit 2% inflation. [pointing a finger in the air, laughing] Which they should not do, because we will hit 2% inflation". Emphasis on "will" was Bullard's. Today, Bullard is concerned. I leave you with this question: Is the falling oil price still "unambiguously good" or does it reflect a rapidly sinking US economy? First Fed Confessional For a stunning video confessional and transcript, please see former Dallas Fed President Richard Fisher Goes to Squawk Box Confessional: "We Frontloaded a Tremendous Market Rally" That rally is blowing up now. Mike "Mish" Shedlock |

| Posted: 15 Jan 2016 10:58 AM PST GDP estimates for fourth quarter will undoubtedly decline after today's series of miserable economic reports. Icing on the miserable cake comes from the commerce department report on Manufacturing and Trade Inventories and Sales for November 2015. Both sales and inventories declined. Sales Down 0.2 percent from October 2015 Down 2.8 percent from November 2014 Inventories Down 0.2 percent from October 2015 Up 1.6 percent from November 2014. Inventories/Sales Ratio The total business inventories/sales ratio based on seasonally adjusted data at the end of November was 1.38. The November 2014 ratio was 1.32.  Synopsis Inventories are up 1.6% from a year ago. Sales are down 2.8% from a year ago. That inventory build was unwarranted, and no doubt inspired by a lot of cheerleading by the Fed about the strength of the US economy. So here we are once again with another recessionary looking inventory-to-sales ratio. The chart reflects November. Earlier today we learned December Retail Sales were Negative. Expect another bad looking chart next month. Mike "Mish" Shedlock |

| Producer Prices Decline More Than Expected, Services Disappoint; Oil Approaches $29 Posted: 15 Jan 2016 09:54 AM PST Producer prices are down again this month followed by an unexpected rise last month. If oil prices stick, expect more of the same next month. Crude Weekly Chart Crude is down $1.80 today, another 5.77%, to a new interim low of $29.28. The session is not over yet so it remains to be seen if today is the first close below $30 since 2003. Producer Prices Decline More Than Expected The Econoday Consensus Estimate was -0.1%, and the actual headline number -0.2%. The producer price-final demand headline in December fell 0.2 percent, nearly reversing November's 0.3 percent increase which now, regrettably, looks like an upside outlier. Year-on-year, the headline is down 1.0 percent. The ex-gas ex-food core rate did rise, but only 0.1 percent while the year-on-year rate is down 2 tenths in the month to only plus 0.3 percent. The ex-gas ex-food ex-services headline is up 0.2 percent with the year-on-year rate unchanged, also at plus 0.3 percent.Services Disappointment Bloomberg reports "Services are the disappointment in this report, unchanged in the month following November's 0.5 percent bounce..." Bloomberg has an error. The services component rose 0.1%. Let's dive into the BLS PPI Report to verify. Final Demand Goods: The index for final demand goods moved down 0.7 percent in December, the sixth consecutive decrease. Over three-quarters of the December decline can be traced to prices for final demand energy, which fell 3.4 percent. The index for final demand foods decreased 1.3 percent. Conversely, prices for final demand goods less foods and energy inched up 0.1 percent.Prices for services related to securities brokerage and dealing jumped 30.3 percent. How inspiring. Mike "Mish" Shedlock |

| Industrial Production Numbers and Revisions Shockingly Bad; Autos Have Peaked Posted: 15 Jan 2016 08:53 AM PST Not only was December industrial production an awful -0.4%, November was revised lower from -0.6% to -0.9%. Not to fear, economists blame the weather for much of the decline. The Econoday Consensus Estimates for industrial production and manufacturing were -0.2% and +0.0% respectively. The actual results were -0.4% and -0.1%. December was not a good month for the industrial economy as industrial production fell a sharper-than-expected 0.4 percent. Utility output, down 2.0 percent, declined for a third straight month reflecting unseasonably warm temperatures. Mining, reflecting low commodity prices and contraction in energy extraction, has also been week, down 0.8 percent for a fourth straight decline. Turning to manufacturing, which is the most important component in this report, production fell 0.1 percent for a second straight month (November revised downward from an initial no-change reading).Index of Industrial Production  It appears the weather has been bad for 10 out of the last 12 months. Industrial Production Numbers  Above table from the Federal Reserve Industrial Production and Capacity Utilization Report. Spotlight on Auto Sector For most of 2015, I had been saying that auto sales were not sustainable. Over the past two months we started to see solid evidence of that viewpoint. I commented on varying auto reports, some good, some bad, on January 5, in December US New Car Sales "Down, Exceptionally Weak" Says Bloomberg; WSJ Says Up and Strong. Those saying December sales were strong failed to take into consideration the number of selling days. Looking ahead, manufacturers have spoken: December vehicle production was down 1.7 percent following November's 1.5 percent decline. The last five months for motor vehicles and parts production look like this: -5.1 August, +0.5% September, +1.1% October, -1.5% November, -1.7% December. Autos have peaked. Mike "Mish" Shedlock |

| Empire State Manufacturing Index Posts Horrific -19.37, Lowest Reading Since April 2009 Posted: 15 Jan 2016 07:59 AM PST Economic data today was awful, at best. Retail Sales Were Negative, and that was arguably the best report. Let's now take a look at the other reports starting with Empire State Manufacturing. The Econoday Consensus estimate was for a slight improvement to -4 from a November reading of -4.59. The actual result was -19.37 with the lowest economic estimate -7.50. The contraction in factory activity in the New York manufacturing region, which began way back in August, unfortunately is picking up a lot of steam this month, at minus 19.37 for the January headline which is the lowest reading since April 2009. New orders, at minus 23.54, are contracting for an eighth straight month and at the sharpest pace since March 2009. Unfilled orders, at minus 11.00, are in an even deeper string of contraction. Employment, at minus 13.00, is down for a sixth straight month as is the workweek, at minus 6.00. And there's a crumbling going on in the 6-month outlook which, at 9.51 is still in the positive column but shows the least optimism since way back in March 2009. This report is grim and offers an initial look at January's factory activity which, based on these results, appears to be getting hit by global concerns.Empire State Manufacturing Index  Mike "Mish" Shedlock |

| December Retail Sales Negative; Other Economic Data Horrid Posted: 15 Jan 2016 07:42 AM PST Despite glowing reports of last minute Christmas sales, none of which I believed, December retail sales are best described as awful. Apparel was a standout, down 0.9%. The surprise here is that nobody blamed the weather. The Econoday Consensus Estimate was flat, and the result was not that far off at -0.1%, but the details were awful. Retail sales proved disappointing in December, down 0.1 percent in a headline that is not skewed by vehicles or even that much by gasoline. Ex-auto sales also fell 0.1 percent while the core ex-auto ex-gas reading came in unchanged which is well below both expectations as well as low-end expectations. The Beige Book yesterday warned us about weak apparel sales which in this report fell a very steep 0.9 percent, in a decline that likely reflects more than just import-price contraction. The general merchandise category, which is very large, fell 1.0 percent in the month. Electronics & appliances also show contraction.There was a slew of economic reports today. This was arguably the best one! Empire State Manufacturing was shockingly bad as was industrial production. Details coming up. Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment