Mish's Global Economic Trend Analysis |

- Judge Rules Stockton CA Bankruptcy is Valid, City Acted in Good Faith

- Cash Cow: Of the 50 Largest US Companies, Who has the Cash? Who has the Debt?

- China PMI Shows Modest Improvement

| Judge Rules Stockton CA Bankruptcy is Valid, City Acted in Good Faith Posted: 01 Apr 2013 12:50 PM PDT Today a judge ruled that the city of Stockton California is indeed bankrupt and that the city acted in good faith. Creditors asked the judge to void the bankruptcy, saying the city could raise taxes instead. I have been watching this story for a while. Here is some background on the Stockton bankruptcy as reported by Arizona Central. By outward appearances, Stockton, a city of nearly 300,000 on the Sacramento-San Joaquin River Delta, seemed in the mid-2000s to be emerging from decades of struggle.City Acted in Good Faith Today, Bloomberg reports a Judge Decided City Acted in Good Faith, Creditors Didn't The judge in a trial over whether the city of Stockton, California, can stay in bankruptcy said he found that the city negotiated in good faith with its creditors, and that the creditors didn't.This was a good ruling. The city is of course bankrupt and taxpayers should not have to pay for it more than they already have. Once again the main problem was untenable salaries for public unions and city workers. The housing crash simply brought the crisis to a head sooner. In addition to reduced healthcare benefits, the pension plan should be scrapped as well, but don't expect city officials to cut their own throats no matter how much they deserve it. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

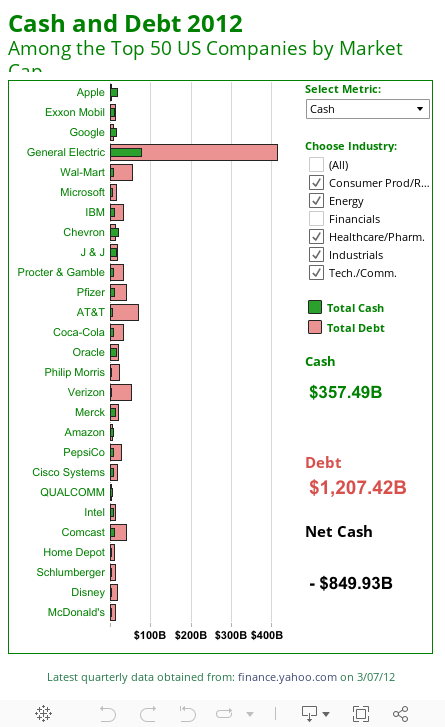

| Cash Cow: Of the 50 Largest US Companies, Who has the Cash? Who has the Debt? Posted: 01 Apr 2013 08:37 AM PDT Here's the question of the day: How much actual cash is on hand at corporations? Fed by glowing reports from sell-side analysts, most investors are unaware that except for a handful of companies, there is no cash, only debt. Even counting short-term investments there is surprisingly little cash on hand. Courtesy of Mike Klaczynski at Tableau Software please consider the latest update to my periodic "Cash Cow" interactive report.  The data for this sheet is from Yahoo!Finance. Scroll over any of the bars (not the company name) to see more details. Cash is a liability not an asset for banks, so I left off financial corporations in the default map. Certainly the $277 billion in cash on hand at Bank of America is not a sign of genuine strength or profitability. As you can see, actual cash on hand at non-financial corporations is a net negative $850 billion. Five Cash Cows With Genuine Cash

The grand total of actual available cash (at the five companies that have any) is $39.71 billion. To add in short-term investments, click on the Select Metric drop-box that looks like this:  Here are the results. 10 Cash Cows Counting Short-Term Investments

Net Negative Cash Counting short-term investments, net corporate cash of the 50 largest companies is negative $543.67 billion. Total cash of the 10 companies that have positive balance sheet cash (counting short-term investments as a cash equivalent) is $216.05 billion. This is a far cry from the $trillions in sideline cash we are told is ready to come pouring into the market any time now. The facts of the matter are:

Yet, the concept of "sideline cash" as widely believed and highly touted by mainstream media is mathematically impossible. It is possible however, for a corporation to use its cash to buy back shares, but in that case, sideline cash will be transferred to another account (frequently the cash account of an insider who is bailing). Recall that investors wanted Apple to buy back shares last Autumn, thinking they were undervalued at $700. Today's price is $435. Had Apple been foolish enough to buy back shares when everyone seemed convinced the next stop was $1000, Apple's share price would undoubtedly be lower today, reflective of the amount of cash it wasted on buybacks. 2009 and 2010 provided excellent opportunities for corporations to buy back shares. Bargains have long since vanished. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| China PMI Shows Modest Improvement Posted: 31 Mar 2013 11:16 PM PDT The HSBC China Manufacturing PMI shows Modest improvement in operating conditions. After five months of recovery and renewed stimulus in China, the PMI index has crawled back above the break-even 50 mark. Yes, this is a "modest improvement" but the stimulus and infrastructure spending that is driving the improvement are unsustainble. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment